Background of the case

In a recent ruling, the Supreme Court (“The Hon’ble Court”) in the case of M/s Jindal Equipment Consultancy Services Ltd1 (“the assessee” or “the Company”) adjudicated a batch of appeals concerning the taxability of shares received by shareholders upon amalgamation, specifically where the shares of the amalgamating company were alleged to be held as stock-in-trade. The dispute pertained to Assessment Year (AY) 1997–98 and examined the interplay between Section 47(vii) of the Income-tax Act, 1961 (“the Act”) and Section 28 of the Act.

Facts of the case

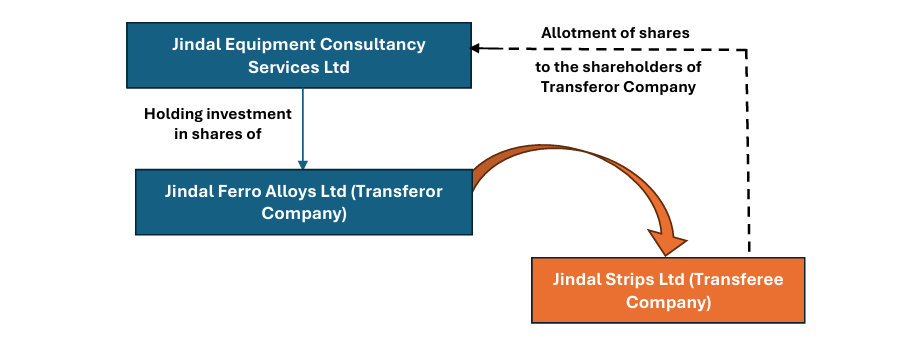

- The appellants were investment companies of the Jindal Group, holding shares in operating companies including Jindal Ferro Alloys Limited (JFAL) and Jindal Strips Limited (JSL) as part of promoter holding (controlling interest). These shares were reflected as investments in their balance sheets.

- Pursuant to a court-sanctioned scheme of amalgamation approved by orders dated 19 September 1996 and 03 October 1996, JFAL was amalgamated with JSL. The appointed date was 01 April 1995 and effective date was 22 November 1996.

- Under the exchange ratio, shareholders of JFAL received 45 shares of JSL for every 100 shares of JFAL.

- The appellants claimed exemption under Section 47(vii) by treating the JFAL shares as capital assets.

- The Assessing Officer considered the JFAL shares as stock-in-trade, denied Section 47(vii) exemption, and taxed the receipt of JSL shares as business income, computed with reference to market value. CIT(A) upheld the same.

- The ITAT allowed the assessees’ appeals, holding that no profit accrues unless there is sale/transfer for consideration and relied on Commissioner of Income Tax, Bombay v. Rasiklal Maneklal (HUF) and others2 to conclude no taxable transfer occurred.

- The Delhi High Court reversed the ITAT and remanded the matter to ITAT, holding:

- If shares were capital assets, amalgamation constitutes a “transfer” (though exempt u/s 47(vii)); and

- If shares were stock-in-trade, the difference could be taxable as business income u/s 28.

- Aggrieved by the above, the assessee filed an appeal with the Supreme Court.

Key Issues

- Whether the High Court exceeded its jurisdiction by opining on taxability under Section 28 for shares held as stock-in-trade, when the substantial question of law formally framed concerned only whether any “transfer” takes place on receipt of shares on amalgamation.

- Whether substitution of stock-in-trade shares of the amalgamating company by shares of the amalgamated company, pursuant to a court-sanctioned amalgamation, itself constitutes a taxable “profit and gain of business or profession” under Section 28, even in the absence of a conventional sale or exchange.

- If such substitution can be taxable, at what point does taxability arise (appointed date, date of court sanction, or actual allotment), and what conditions (real income, commercial realisability, definite valuation) must be satisfied.

Key Takeaways

1. Jurisdiction under Section 260A

- The Supreme Court held that the High Court did not transgress Section 260A, since the question of taxability under Section 28 was “incidental or collateral” to the substantial question already framed and arose directly from the Tribunal’s failure to determine the nature of the holding.

- It further held that formal framing of a separate substantial question is not mandatory where the issue goes “to the very root of the matter” and the parties were fully heard on the point before the High Court.

- The Hon’ble Court emphasized that the requirement of framing substantial questions of law is intended to ensure fairness and clarity, but it cannot be applied in a manner that defeats adjudication of the real dispute when the issue is evidently part of the matter in appeal.

- The remand was upheld as the High Court did not itself assess income under Section 28, but only held that without determining whether shares were capital assets or stock-in-trade, taxability could not be adjudicated.

2. Section 28 applicability for stock-in-trade cases

- The Hon’ble Court clarified that Section 47(vii) grants exemption only for transfers of capital assets on amalgamation and has no application where the surrendered shares are held as stock-in-trade.

- The Hon’ble Court categorically held that Section 28 is a wide charging provision, which does not require a “transfer”, “sale” or “exchange” as a pre-condition, unlike Section 45 which is confined to capital assets.

- It was reiterated that profits and gains of business may arise “whether in cash or in kind”, and the definition of “transfer” under Section 2(47) is irrelevant for determining business income.

- The judgment clarifies that amalgamation is a statutory substitution, not a bilateral exchange; however, absence of an “exchange” does not immunise the transaction from Section 28.

- The Hon’ble Court rejected the Tribunal’s view that no income can arise unless shares are sold, holding that such an approach unduly restricts Section 28, which is designed to capture real business profits in diverse commercial forms.

3. Timing of taxability

- The Hon’ble Court held that no taxable business income can be said to arise merely on the “appointed date” mentioned in the scheme of amalgamation, or even on the date when the scheme is sanctioned/approved by the Court.

- Mere legal substitution of rights under a scheme does not by itself amount to a commercial realisation of profit, particularly in cases where the assessee has not yet received the allotment of new shares or obtained an asset that can be objectively valued and dealt with.

- Accordingly, The Hon’ble Court held that the point of taxation (if at all applicable) arises only when the assessee actually receives the new shares of the amalgamated company, i.e., on the date of allotment/receipt.

4. Real income and factual determination

- The Supreme Court held that mere substitution of shares does not automatically give rise to taxable income; taxability depends on whether the transaction results in “real and presently realisable commercial benefit”.

- The Hon’ble Court identified three critical conditions:

- the old stock-in-trade must cease to exist,

- the substituted shares must have a definite and ascertainable value, and

- the assessee must be in a position to commercially realise such value.

- The Hon’ble Court expressly held that where substituted shares are not freely tradable (for eg in case of shares of closely held companies), subject to lock-in, or lack a ready market, the principle of real income bars taxation at the stage of amalgamation, deferring taxability until actual sale.

- Furthermore, The Hon’ble Court emphasised that valuation is an essential element of real income, observing that taxability under Section 28 can arise only where the substituted shares possess a “definite and ascertainable value”.

- Where the allotted shares have a readily determinable market value, such valuation certainty contributes to the existence of a presently realisable commercial advantage, whereas absence of a reliable market or valuation renders any purported gain notional and unreal at the stage of amalgamation.

- Hence, The Hon’ble Court ultimately held that taxability under Section 28 depends upon whether, on the allotment of shares, the assessee received a benefit that is real, measurable, and commercially realisable, and since this required deeper factual verification, the matter was appropriately remitted for fresh consideration.

Conclusion

The Supreme Court held that receipt of shares of the amalgamated company in substitution of shares of amalgamating entity held as stock-in-trade can constitute taxable business income u/s 28, provided the shares received are realisable in money and capable of definite valuation. The taxable event, however, arises only on allotment of new shares, and not at earlier stages such as appointed date or court sanction. As factual determination was still required (nature of holding and commercial realisability), the matter was remitted to the Tribunal for fresh adjudication.

Kretha Comments

This ruling clearly separates amalgamations involving capital investments, which continue to enjoy exemption under Section 47(vii), from amalgamations involving trading assets, which may give rise to tax under Section 28. The Supreme Court has clarified that business income can arise even where consideration is received in kind, but only when it results in a real and commercially realisable benefit.

The key principles from the decisions are as under:

- The Hon’ble Court has held that while merger involving capital investments shall continue to have exemption, transfer of shares of amalgamating (transferor) entity held as stock in trade is taxable.

- However, if the shares received on merger itself is subject to lock-in or not freely transferable, like in the case of closely held companies for which no open market exist to ascribe a fair disposable value, it cannot be said to be taxable on receipt of shares on merger.

- The taxation, in such a case, shall be deferred and shall trigger on ultimate sale of shares received on merger. Jindal Equipment Consultancy- S…

Points to consider while structuring a merger are:

- In a merger transaction it would need to be evaluated if the investment in the transferor / amalgamating entity is recorded as stock in trade.

- Further, whether the shares received on merger are freely transferable or not subject to any lock-in.

- The ruling could also have consequences in the hands of individuals / broking entities if they own any investments as stock in trade for eg. in the case of shares of listed entity held as stock in trade.

Leave A Comment