Background of the case

In a landmark judgment, the Supreme Court of India, in the case of Tiger Global International II Holdings & Ors.1 (2026 INSC 60), has settled several long-standing controversies relating to taxation of indirect transfers, treaty shopping, the evidentiary value of Tax Residency Certificates (“TRCs”), and the scope and application of General Anti-Avoidance Rules (“GAAR”).

The ruling arises from the high-profile exit of Tiger Global from Flipkart pursuant to Walmart’s acquisition of Flipkart Group and is one of the most significant international tax decisions post the Vodafone amendments. The judgment clarifies the interaction between domestic anti-avoidance provisions and tax treaties and significantly reshapes the risk landscape for foreign portfolio and private equity investors investing into India through intermediate jurisdictions such as Mauritius.

Transaction Structure

Facts of the case:

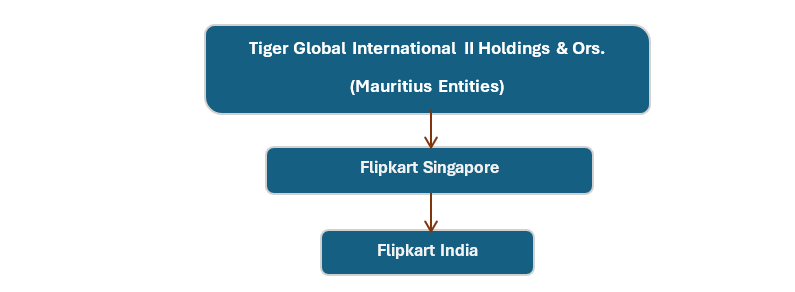

- Tiger Global International II, III and IV Holdings (‘the Applicants’ or ‘the Assessee’) were incorporated in Mauritius and held shares in Flipkart Singapore.

- Flipkart Singapore, in turn, held controlling interests in Indian operating companies, which constituted the primary source of value.

- Tiger Global acquired its investments during 2011–2015 but exited in 2018 as part of Walmart’s acquisition of Flipkart.

- The Applicants approached the Authority for Advance Rulings (“AAR”) seeking a ruling that capital gains arising from the sale of shares of Flipkart Singapore were exempt from Indian tax under Article 13(4) of the India–Mauritius DTAA.

- The AAR rejected the applications at the threshold under proviso (iii) to Section 245R(2), holding that the arrangement was prima facie designed for tax avoidance.

- The Delhi High Court set aside the AAR’s rejection and remanded the matter for adjudication on merits.

- The Revenue appealed to the Supreme Court.

Key Issues

- Whether the AAR was justified in rejecting the advance ruling applications at the threshold under proviso (iii) to Section 245R(2) on the ground that the transaction was prima facie designed for avoidance of income-tax.

- Whether (post statutory changes) a TRC is conclusive for treaty residence/entitlement or whether the Revenue can still examine residence, control/management and treaty abuse while testing the Section 245R(2) bar.

- Whether GAAR (Chapter X-A), including the Rule 10U framework and its “grandfathering”, could apply to deny treaty benefits where the tax benefit is obtained after 01.04.2017 even if the underlying investments were acquired earlier.

- Whether Article 13 of the India–Mauritius DTAA protects indirect transfers of shares.

Key Takeaways

- AAR’s threshold bar under Section 245R(2)(iii)

- The Supreme Court affirmed that the AAR can reject an application at the admission stage where the transaction appears prima facie designed for avoidance of income-tax.

- At the admission stage, the AAR is not required to conduct a detailed trial or final adjudication. The burden lies on the taxpayer to demonstrate that the arrangement is not impermissible within the meaning of Section 96.

- It held that, on the facts, the AAR was right to treat the structure/transaction as a tax avoidance arrangement and therefore refuse to answer on merits due to the statutory bar in proviso (iii) to Section 245R(2).

- TRC is an eligibility condition, not conclusive proof

- The Court held that post-amendments, a TRC by itself is not “sufficient” to establish treaty residence/eligibility, and earlier circular/jurisprudence must be read in the context of the changed statutory regime (including Section 90(2A), Section 90(4) and Chapter X-A).

- CBDT Circulars, including Circular No. 789, cannot override statutory amendments or curtail the scope of GAAR.

- Consequently, the Revenue is no longer precluded from investigating the actual “head and brain” or centre of management of an entity, despite the possession of a valid certificate.

- It held that revenue authorities are entitled to examine whether the entity claiming treaty benefits is a genuine resident and the beneficial owner of income, having regard to control, management, commercial substance and economic reality.

- GAAR and limits of “grandfathering”

- The Court recognised that GAAR applies to the relevant assessment year and emphasised that “grandfathering” is not absolute where the tax benefit from an arrangement is obtained after the specified cut-off (i.e., transfers/benefits post 01.04.2017 can still attract GAAR scrutiny under the Rule 10U framework).

- It underscored that an assessee cannot succeed merely by pointing to pre-2017 acquisition if the arrangement yielding tax benefit (including the sale/exit steps) occurs later and is found to be impermissible.

- Scope of Article 13 of the India-Mauritius DTAA

- The Supreme Court held that Explanation 5 to Section 9(1)(i) squarely applies to the transaction. Since Flipkart Singapore derived substantial value from assets located in India, the gains arising from the sale of Flipkart Singapore shares constituted income deemed to accrue or arise in India.

- The Supreme Court noted that while direct transfers of shares acquired after 1 April 2017 are governed by the source-based rules of Article 13(3A), indirect transfers fall under the residuary rule of Article 13(4).

- Under Article 13(4), taxing rights are generally allocated to the State of residence (Mauritius). However, the Supreme Court clarified that this treaty protection is not absolute and subject to alienator being a resident.

- The Court emphasised that tax treaties are intended to prevent double taxation and not to facilitate double non-taxation or treaty abuse.

Conclusion

The Supreme Court allowed the Revenue’s appeals, set aside the Delhi High Court judgment, and upheld the AAR’s rejection of advance ruling applications as barred by proviso (iii) to Section 245R(2) due to prima facie tax avoidance. The ruling significantly bolsters the tax authorities’ power to scrutinise holding structures for commercial substance and impermissible tax avoidance (including under GAAR), while confirming that mere possession of a TRC does not shield taxpayers from such examination.

Kretha Comments

The Hon’ble Supreme Court’s decision decisively marks a shift from form-driven treaty interpretation to a substance-based anti-avoidance regime. The judgment confirms that indirect transfers deriving value from India are taxable, that TRCs do not confer automatic treaty protection, and that GAAR has wide amplitude even in respect of legacy investments yielding post-2017 tax benefits.

For foreign investors, the ruling underscores the critical importance of real economic substance, demonstrable commercial purpose and robust governance in holding structures. Treaty-based exits from India will now be closely scrutinised through the lens of GAAR and anti-abuse principles.

- CIVIL APPEAL NO. 262 OF 2026 ↩︎

Leave A Comment