Background

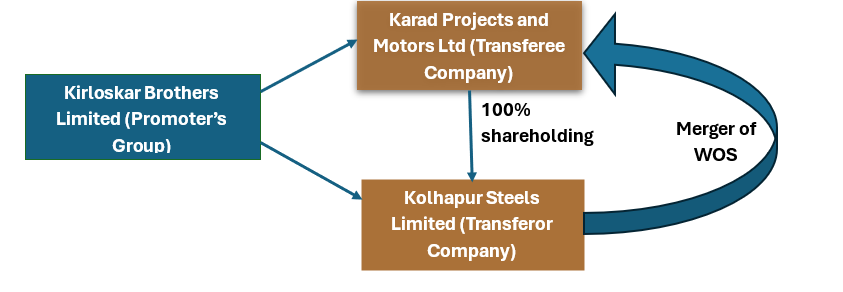

In a recent case, a petition was filed by Kolhapur Steel Limited1 (“the Company” or “Transferor Company”) before the National Company Law Tribunal (“NCLT” or “The Tribunal”), Mumbai Bench, seeking approval for the scheme of amalgamation between the Company and Karad Projects and Motors (“Transferee Company”) under Sections 230 to 232 of the Companies Act, 2013. Both entities form part of the same promoter’s group i.e. Kirloskar Brothers Limited (KBL) Group.

The merger was proposed as part of an internal group restructuring exercise intended to consolidate the Group’s manufacturing operations, achieve operational and managerial efficiencies, and utilize the surplus industrial land held by the Transferor Company at Kolhapur for the Transferee’s future expansion. While the Income Tax Department questioned that the merger was driven primarily to claim carried‑forward losses of the Transferor Company, the Tribunal observed that mergers among the group companies, aimed at reviving the business of Transferor Company, should not be assumed as a device to avoid tax even if as a consequence of merger there is a tax benefit as per the law.

Facts of the case

- The Transferor Company is engaged in the manufacture of steel castings, forgings, and fabrication components.

- The Transferee Company manufactures electric motors, rotors, and pumps. Both entities operate within complementary industrial segments of the parent group.

- The Scheme of Amalgamation provides that, with effect from the Appointed Date of 03 October 2024, the entire business undertaking of the Transferor Company including all its assets, properties, investments, contracts, permits, and employees shall stand transferred to and vest in the Transferee Company as a going concern.

- The Transferor Company had brought-forward business losses of INR 83.33 crore and unabsorbed depreciation of INR 13.18 crore, in respect of which the Income Tax Department raised detailed objections. The Department alleged that the Scheme was structured primarily to evade taxes by enabling the Transferee Company to offset its gains against these accumulated losses and unabsorbed depreciation, thereby substantially reducing its tax liability and causing potential loss of revenue to the public exchequer.

Key Issues

- Whether the Scheme of Amalgamation was structured with the primary objective of availing set-off of accumulated business losses and unabsorbed depreciation of the Transferor Company under Section 72A of the Income-tax Act, 1961, and therefore amounted to a “colourable device” for tax avoidance.

- Whether the provisions of the General Anti-Avoidance Rules (GAAR) under Chapter X-A of the Income-tax Act, 1961, were attracted to the proposed merger, considering the Department’s contention that the transaction lacked commercial substance and resulted in a tax benefit.

- Whether the proposed Scheme could be said to be contrary to “public interest” under Section 230(1) and (6) of the Companies Act, 2013, merely because it resulted in incidental tax advantages to the Transferee Company.

Key Takeaways

1. Genuine Business Purpose – Tax Efficiency Alone Does Not Constitute Avoidance

- The Tribunal held that mere existence of accumulated losses in the Transferor Company does not automatically convert a merger into a tax-avoidance device.

- The Applicants established that the merger was driven by genuine business objectives, including stabilising the financially distressed Transferor Company, eliminating duplicate costs, improving credit strength, reducing compliance risks, and achieving operational synergies.

- The Tribunal relied on:

- Union of India v. Azadi Bachao Andolan2 – legitimate tax planning is not tax evasion.

- CIT v. Walfort Share and Stock Brokers Pvt. Ltd.3 – tax benefits available under law cannot be denied merely because they reduce tax liability.

- Sadashiva Sugars Ltd (Karnataka HC)4 – Section 72A does not bar amalgamation of loss-making companies.

- Bhoruka Engineering Industries Ltd. v. DCIT5 and AMNS Khopoli Ltd6 & PCA Motors Pvt Ltd (NCLT Mumbai)7 – tax benefits do not render a merger colourable if commercial intent exists.

- The Tribunal clarified that business restructuring aimed at preventing loss of production, employment, and capital cannot be deemed a tax-avoidance scheme merely due to resulting tax benefits.

2. Applicability of GAAR

- The Assessee explained that GAAR can only be invoked through the procedure in Section 144BA, requiring referral to an Approving Panel. No such process was initiated by the Income Tax Department.

- Thus, GAAR implications cannot be presumed during NCLT proceedings without following statutory procedure.

- The Tribunal further observed that the merger demonstrated clear commercial substance and therefore fell outside GAAR applicability.

3. Public Interest and Economic Substance

- The Tribunal held that the ability of the Transferee Company to claim Section 72A benefits does not make a merger contrary to public interest.

- The consolidation of manufacturing operations, improved use of industrial land, and overall economic stability of the group were seen as indicators of genuine commercial purpose.

- The incidental tax benefit did not compromise public interest.

Conclusion

The Tribunal concluded that the merger was driven by genuine commercial considerations namely, consolidation of manufacturing operations, efficient utilisation of assets, and revival of a loss-making unit and not by any intent to evade taxes. The mere availability of benefits under Section 72A of the Income-tax Act, 1961 was held not to invalidate the Scheme, since such benefits are legislatively intended to promote business reorganisations and economic revival.

The Tribunal reaffirmed that commercial intent, transparency, and statutory compliance are the decisive tests in determining the legitimacy of a merger and that lawful tax efficiencies do not detract from a genuine business restructuring.

Kretha Comments

This decision is a significant affirmation of the principle that tax efficiency, when incidental to a genuine business reorganisation, does not equate to tax avoidance. The ruling underscores the importance ofcommercial substance and documented business rationale in defending group restructurings against allegations of tax evasion or public interest violations.

From an advisory perspective, this case provides valuable guidance on caution points to be considered in merger cases involving any tax benefits like carry forward of accumulated losses or unabsorbed depreciation. It highlights the need for careful detailing of the justification of commercial intent, and adherence to both corporate and tax compliance frameworks.

Leave A Comment