Background of the Case

In a recent ruling, the Chennai Income Tax Appellate Tribunal (hereinafter referred to as “the Tribunal” or “ITAT”), in the case of VS Trust1 (“the assessee” or “the trust”) decided on the taxability of property received by a private trust from its settlor under Section 56(2)(x) of the Income-tax Act, 1961 (“IT Act”). The dispute revolved around whether shares contributed by the settlor to the trust could be taxed as income from other sources or whether the transaction qualified for the statutory exemption available when property is received by a trust established solely for the benefit of the relatives of an individual.

The Assessing Officer (“AO”) treated the shares contributed to the trust as taxable income under Section 56(2)(x), alleging that the trust was not exclusively created for the benefit of relatives. The assessee trust challenged the addition before the appellate authorities, ultimately leading to adjudication by the ITAT.

Trust Structure

Facts of the Case

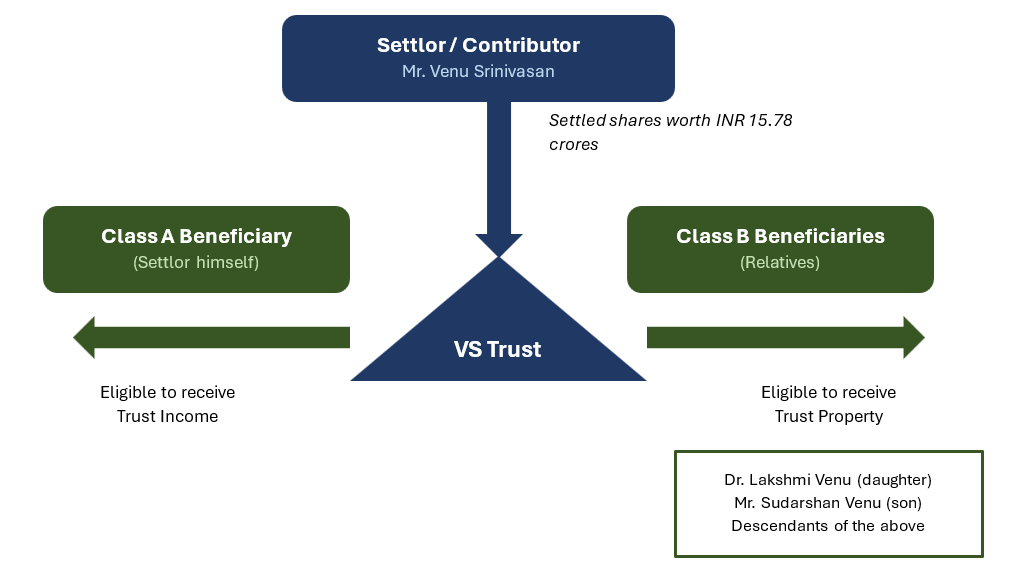

- VS Trust is a private trust settled on 01 September 2021 by Mr. Venu Srinivasan (“the settlor”) for the benefit of his family members.

- During AY 2022-23, the trust received shares worth INR 15.78 crore as contribution from the settlor.

- The assessee claimed that the receipt was not taxable in view of the exemption under clause (X) of the proviso to Section 56(2)(x), which excludes property received by a trust created solely for the benefit of relatives of the individual.

- The AO, upon scrutiny, noted that Clause 5.2 of the original trust deed permitted the trustees to add any entity majority-owned or controlled, directly or indirectly, by the relatives of the Settlor, as a beneficiary. The AO held that such a provision could result in minority interests accruing to non-relatives and, accordingly, the trust could not be said to have been created exclusively for the benefit of relatives and added the value of shares as income under Section 56(2)(x).

- Additionally, the AO also added INR 12 crore, representing advance tax erroneously paid by the settlor in the PAN of the trust, treating it as income under Section 56(2)(x).

- Before the CIT(A), the assessee contended that a supplemental trust deed dated 03 March 2022 (effective from inception) had replaced Clause 5.2, removing the provision allowing addition of such entities and restricting beneficiaries only to relatives.

- The CIT(A) acknowledged the amended deed but held the amendment to Clause 5.2 to be invalid and upheld the addition. The trust then appealed before the ITAT.

Key Issues

- Whether the shares contributed by the settlor to the assessee trust were taxable under Section 56(2)(x) as income from other sources.

- Whether the supplemental trust deed amending the beneficiary clause was legally valid.

- Whether the assessee trust could be regarded as a trust created solely for the benefit of relatives of the settlor, thereby qualifying for the exemption under clause (X) of the proviso to Section 56(2)(x).

Key Takeaways

- Applicability of Section 56(2)(x)

- Section 56(2)(x) provides that where any person receives property without consideration and the fair market value exceeds INR 50,000, the entire value is taxable under the head “Income from Other Sources.”

- However, the proviso to Section 56(2)(x) excludes property received by a trust from an individual where the trust is created solely for the benefit of the relatives of such individual.

- Therefore, if the statutory conditions of the exemption are satisfied, the receipt of property by such trust cannot be brought to tax under Section 56(2)(x) even if the property is transferred without consideration.

- Validity of the Amendment to the Trust Deed

- The ITAT held that Clause 8.1.2(b) of the original trust deed, while prohibiting amendments that would result in the Settlor regaining power over trust property, affect the power of disposition over trust property or alter the objects of the trust, did not restrict amendments to the beneficiary clause.

- The CIT(A)’s interpretation that Clause 5.2 could not be amended was found to be without any textual or legal foundation.

- The ITAT further noted that Clause 8.1.2(d) of the original trust deed expressly empowered the trustees to add or remove any beneficiary. The amendment to Clause 5.2 through the supplemental deed dated 03.03.2022 was accordingly held to be valid and effective from the inception of the trust.

- Whether the Trust was Created Solely for the Benefit of Relatives

- The beneficiaries listed in the supplemental trust deed included the settlor, his son, daughter, and their lineal descendants, all of whom fall within the definition of “relative” under the IT Act. The clause of the original trust deed that permitted addition of any entity majority-owned or controlled, directly or indirectly, by the relatives of the Settlor, as a beneficiary was thereby removed. Hence, the question of validity of such a clause in the original trust deed for the purposes of Section 56(2)(x) was not examined by the Tribunal.

- The Tribunal emphasized that the actual beneficiaries of the trust must be examined, rather than relying on speculative or hypothetical possibilities of non-relatives benefiting in the future.

- Clause 5.2 as amended only permitted the trustees to remove (and not add) beneficiaries, and no provision existed in the amended deed for any non-relative to benefit from the trust.

- The assessee trust was therefore found to have been established solely for the benefit of the relatives of the Settlor.

Conclusion

The Chennai ITAT ultimately held that the assessee trust was established exclusively for the benefit of the relatives of the settlor, and therefore the contribution of shares by the settlor qualified for the specific exemption provided under clause (X) of the proviso to Section 56(2)(x) of the IT Act. The Tribunal rejected the Revenue’s reliance on the earlier wording of the trust deed and recognized the validity of the supplemental amendment, which clarified that the beneficiaries were restricted to relatives of the settlor.

Accordingly, the Tribunal concluded that the foundational basis for invoking Section 56(2)(x) did not exist, as the statutory conditions for exemption were satisfied. On this reasoning, the ITAT set aside the findings of the lower authorities and directed deletion of the addition of INR 15.78 crore, thereby allowing the appeal of the assessee trust.

Kretha Comments

This decision provides important clarification regarding the scope of Section 56(2)(x) in the context of private family trusts. The ruling emphasizes that the exemption for trusts benefiting relatives should be interpreted based on the substantive purpose and actual beneficiary structure of the trust, rather than speculative interpretations of potential future beneficiaries.

The judgment also highlights the significance of proper interpretation of trust deeds and supplemental amendments, confirming that valid amendments which reinforce the original objects of the trust cannot be disregarded by tax authorities.

From a structuring perspective, the ruling reinforces that family trusts structured exclusively for relatives can receive property contributions from the settlor without triggering taxation under Section 56(2)(x), provided the trust deed clearly restricts beneficiaries to qualifying relatives.

- TS-244-ITAT-2026(CHNY) ↩︎

Leave A Comment