Background

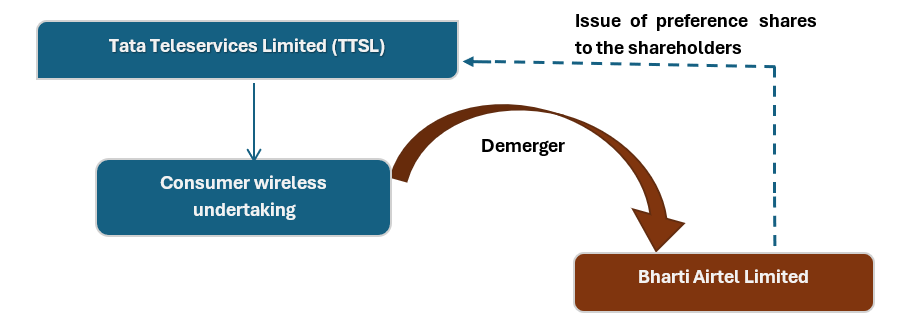

In a recent ruling, the Delhi Income-tax Appellate Tribunal (“the Tribunal”), in the case of Bharti Airtel Limited1 (“the Company”), examined tax implications arising from the demerger of the consumer wireless business undertaking of Tata Teleservices Limited (TTSL) into Bharti Airtel under a scheme of arrangement sanctioned by the NCLT under sections 230–232 of the Companies Act, 2013.

The case underscores significant interpretative issues concerning tax treatment of court-sanctioned restructurings, particularly the distinction between a demerger and a business acquisition. While the ruling deals with several issues, this note is confined to demerger related aspects only such as denial of carry forward of losses and unabsorbed depreciation, and classifying the transaction as business acquisition by treating them as capital expenditure.

Facts of the case

- During the year 2019-20, Bharti Airtel implemented the demerger of TTSL consumer wireless business, pursuant to NCLT approved scheme.

- During assessment, the Assessing Officer (“AO”) examined various issues. While certain disallowances were made, the AO specifically accepted the Company’s claim of the setoff of brought forward losses and unabsorbed depreciation.

- Subsequently, the Principal Commissioner of Income Tax (“PCIT”) invoked revisionary jurisdiction under Section 263 of the IT Act and held that the assessment order was erroneous and prejudicial to the interests of the Revenue. In doing so, the PCIT directed (amongst other things):

- Denial of setoff of brought forward losses and unabsorbed depreciation of TTSL under Section 72A, alleging non-compliance with Section 2(19AA) conditions.

- Taxation of “excess net assets” over consideration under Section 56(2)(x) of IT Act, recharacterizing the transaction as a business acquisition instead of a demerger.

- Aggrieved by the above findings of the PCIT, the assessee filed an appeal before the Delhi Income-tax Appellate Tribunal.

Key Issues

- Eligibility to carry forward and set off losses and unabsorbed depreciation pursuant to a demerger under Section 72A.

- Taxability of alleged income under Section 56(2)(x) of IT Act on excess net assets over consideration in demerger.

Key Takeaways

- Carry Forward and Setoff of Losses and Unabsorbed Depreciation Post Demerger

- In the transaction, Bharti Airtel sought to claim set-off and carry forward of brought-forward business losses of ₹14,585 crore and unabsorbed depreciation of ₹7,147 crore that pertained to the demerged wireless business undertaking of TTSL.

- Nature of Consideration (Redeemable Preference Shares): PCIT noted that under Section 2(19AA)(iv) and (v), for a transaction to qualify as a “demerger”, at least three-fourths of the shareholders of the demerged company (TTSL) should become shareholders in the resulting company (Bharti Airtel) by virtue of the demerger. In the instant case, the scheme sanctioned by NCLT provided for the issue of not equity shares, but redeemable, non-participative, non-voting preference shares to TTSL shareholders. These preference shares were mandatorily redeemable after just 18 months from their issue. According to PCIT, redeemable preference shares of such a short-term, non-participative, and non-voting nature are akin to debt instruments rather than equity participation. Therefore, this did not constitute a genuine “demerger” under the statutory definition, but rather a business acquisition, disqualifying it from Section 72A benefits.

- Tribunal’s view: The Tribunal, while overruling the PCIT, highlighted that there is no such stipulation in Section 2(19AA) or the Companies Act that only equity shares must be issued. The section refers more broadly to “shareholders,” which includes both equity and preference shareholders, as recognized by Section 43 of the Companies Act. The tribunal explained that the law does not prescribe any minimum period for which the allottees of such shares should remain shareholders, nor restrict the type of shares that can be issued, so long as three-fourths in value of the shareholders continue as shareholders in the resulting company immediately post-demerger. The tribunal rejected the PCIT’s importation of subjective requirements not present in the law.

- Therefore, Bharti Airtel was entitled to carry forward and set off the accumulated losses and unabsorbed depreciation.

- Taxability of Alleged Income Under Section 56(2)(x) for Excess Net Assets Over Consideration

- The PCIT had sought to tax ₹1,230 crore as income under Section 56(2)(x) of IT Act, alleging that Bharti Airtel received excess net assets over the consideration paid while acquiring TTSL’s consumer wireless business. This was based on the premise that the scheme was not a demerger but a business acquisition.

- The Tribunal categorically rejected the PCIT’s treatment, holding that the transaction was a valid court-approved demerger, and not an acquisition for consideration.

- Section 56(2)(x) applies exclusively to transfers of “property.” Undertakings transferred via a demerger are specifically not covered under the definition of property for the purpose of this section.

- Moreover, proviso to Section 56(2)(x) under clause (IX) expressly excludes demerger transactions from its scope.

- Importantly, the Tribunal also noted that the PCIT had not issued any specific show-cause notice before making an addition under Section 56(2)(x). By invoking a new source of income without giving the assessee an opportunity to respond, the PCIT acted in violation of principles of natural justice. On this basis too, the addition was held to be unsustainable.

Conclusion

The Tribunal’s ruling in Bharti Airtel resolves critical questions on tax neutrality of demerger and applicability of section 56(2)(x) on business transfer. It confirmed that the NCLT-approved transfer of TTSL’s wireless business was a valid demerger allowing set-off of accumulated losses and rejected the PCIT’s attempt to tax excess net assets over consideration under Section 56(2)(x).

- TS-136-ITAT-2025(Del) ↩︎