Background

In a recent ruling, the Delhi High Court (“the Court”), in the case of PMV Maltings (P) Ltd1 (“the Company” or “the Assessee”), examined the interpretation of Fifth Proviso to Section 32(1) of the Income-tax Act, 1961 (“the Act”), in the context of depreciation claims following a demerger. The assessee acquired two malt production units through a Scheme of Arrangement and recorded goodwill in its books in FY 2013-14, claiming depreciation on it under Section 32(1) of the Act. The matter was examined initially by the Assessing Officer and later by the Delhi Tribunal (“the Tribunal”), which disallowed depreciation on the same for subsequent assessment years by applying the Fifth Proviso to Section 32(1) of the Act.

It is important to note that this summary does not deal with the question of whether goodwill is eligible for depreciation, as that principle was already settled in earlier decisions and subsequent amendment in the Act. The discussion here is confined specifically to the applicability of the Fifth Proviso to Section 32(1) and the period for which it governs the claim of depreciation following a demerger.

Facts of the case

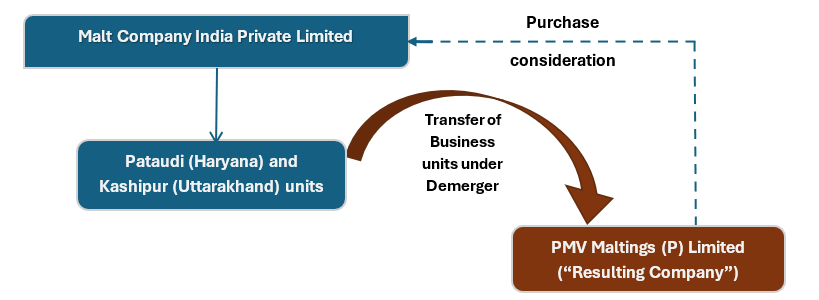

- The Company acquired two malt production units situated at Pataudi (Haryana) and Kashipur (Uttarakhand) from Malt Company India Pvt. Ltd. (MCIPL) under a Scheme of Arrangement approved by the Delhi High Court on 5 October 2012, with 1 April 2013 as the appointed date.

- The difference between the purchase consideration and the net value of assets acquired was recorded in the assessee’s books as goodwill amounting to INR 16.62 crore in Financial Year 2013–14 (corresponding to AY 2014–15).

- The assessee claimed depreciation at the rate of 25 per cent under Section 32(1) on this goodwill for assessment years 2014–15, 2015–16 and 2016–17.

- The Assessing Officer and subsequently the Tribunal accepted that goodwill constitutes an intangible asset eligible for depreciation under Section 32(1), in line with the Supreme Court’s decision in CIT v. Smifs Securities Ltd.2 However, the Tribunal disallowed the depreciation claim for AYs 2015–16 and 2016–17 based solely on the Fifth Proviso to Section 32(1) of the Income-tax Act, 1961, which regulates aggregate depreciation allowable where succession or demerger occurs.

- Aggrieved by this disallowance, the assessee filed an appeal before the Delhi High Court.

Key Issues

- Whether the restriction contained in the Fifth Proviso to Section 32(1) of the Act applies only in the year of succession or continues to limit the claim of depreciation by the resulting company in subsequent assessment years following a demerger.

Key Takeaways

- Applicability of Fifth Proviso to Section 32(1) in subsequent years of demerger

- The Court examined the scope and application of the Fifth Proviso to Section 32(1) and held that the proviso governs only the aggregate depreciation allowable to the predecessor and successor in the year of succession, amalgamation, or demerger.

- The Court observed that the purpose of Fifth Proviso is merely to ensure that in the year of restructuring, the total deduction for depreciation does not exceed the amount that would have been allowable had the restructuring not taken place.

- Since the Scheme of Arrangement between MCIPL and PMV Maltings (P.) Ltd. became effective from 1 April 2013 (AY 2014–15), the Court held that the Fifth Proviso could not have any bearing on the depreciation claimed in subsequent assessment years, namely 2015–16 and 2016–17.

- The Court emphasized that once the succession has taken effect, the resulting company becomes the sole owner of the assets, and there is no longer a question of aggregate depreciation being shared with the predecessor.

- In support of its interpretation, the Court relied upon the following judicial precedents:

- Accordingly, the Court held that the Fifth Proviso to Section 32(1) was relevant only for the assessment year in which the demerger took effect, i.e., AY 2014–15 and had no application to subsequent years.

Conclusion

The ruling of the Delhi High Court clearly delineates the scope of the Fifth Proviso to Section 32(1), confirming that its application is restricted to the year in which the succession or demerger takes place. By setting aside the Tribunal’s order, the Court reaffirmed that once the transfer of assets has taken effect, the resulting company is entitled to claim depreciation. The judgment provides interpretative certainty and ensures consistency in the application of depreciation provisions in cases involving corporate restructuring.

Kretha Comments

This ruling provides clarity on the temporal scope of the Fifth Proviso of Section 32(1). By holding that the proviso applies only in the year of succession, the Court has clarified that its purpose is limited to regulating the aggregate depreciation claim in the transition year and does not impose an ongoing restriction in subsequent years.

It also aligns with judicial precedents from other High Courts, thereby contributing to a uniform and consistent interpretation of the Fifth Proviso across jurisdictions.