Background of the case

In a recent ruling, the Chennai Tribunal (hereinafter referred to as “the Tribunal” or “ITAT”) in the case of Valeo Bayen1 (“the Assessee”) examined the scope and application of Section 47(iv) of the Income-tax Act, 1961 (“the Act”) in the context of an intra-group share transfer by the Assessee to its wholly owned Indian subsidiary.

The dispute centred on two interconnected questions. The first was whether the shares transferred constituted capital assets, given that a portion of the holding had been acquired in close proximity to the date of transfer. The second was whether the transaction, structured as a share sale followed by a fast-track merger under Section 233 of the Companies Act, 2013, amounted to a colourable device designed to remit funds from India without incurring tax.

Facts of the case

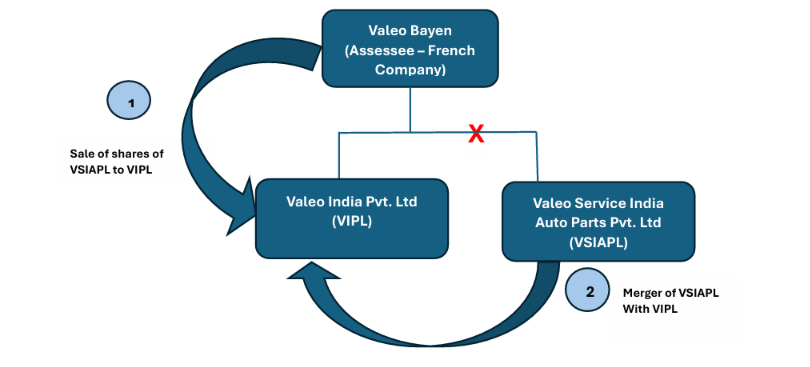

- The Assessee, a French company held 100% of Valeo India Pvt. Ltd. (VIPL) and 99.98% of Valeo Service India Auto Parts Pvt. Ltd. (VSIAPL), both Indian companies. The Assessee classified its shareholding in both entities as investments in subsidiaries under long-term financial assets.

- VSIAPL was originally a joint venture between the Assessee (holding 60%, infused as share capital in 2012 and 2014) and Asia Investment Private Limited (AIPL), an Anand Group entity (40%). Following the failure of the joint venture, the assessee acquired the remaining 40% stake comprising 35,96,000 shares from AIPL in June 2018 at INR 55 per share, making VSIAPL a wholly owned subsidiary.

- On 23 December 2019, the Assessee sold its entire holding in VSIAPL to VIPL for a consideration of INR 64,78,01,960. Following the transfer, VSIAPL was merged with VIPL under the fast-track merger process under Section 233 of the Companies Act, 2013.

- The Assessee claimed the transfer as exempt from tax under Section 47(iv), filed its return of income for AY 2020-21 accordingly, and sought a refund of the taxes withheld.

- The Assessing Officer rejected the Section 47(iv) exemption on the grounds that shares constituted as stock in trade and not capital asset and proceeded to treat the entire consideration as income from other sources.

- Aggrieved by the draft assessment order passed by the Assessing Officer, the assessee filed objections before the Disputes Resolution Panel (DRP), who confirmed the addition made by the Assessing Officer.

- Aggrieved by the above, the assessee appealed to the Tribunal.

Key Issues

1. Whether the shares of VSIAPL held by the Assessee constituted ‘capital assets’ within Section 2(22) of the Act, or whether the subsequent acquisition of the 40% stake in 2018 and its transfer in 2019 recharacterized the entire holding as stock-in-trade.

2. Whether the transfer of shares of VSIAPL to its wholly owned Indian subsidiary VIPL qualified for non-recognition as a ‘transfer’ under Section 47(iv) of the Act, given the statutory conditions of that provision.

3. Whether the Revenue was entitled to question the commercial choice of implementing a group reorganisation through a share transfer followed by a fast-track merger, and treat the transaction as a colourable device or non-genuine arrangement.

4. Whether the AO was justified in rejecting the DCF-based valuation report without identifying specific defects, and whether post-merger accounting disclosures could constitute evidence of a sham transaction.

Key Takeaways

- Characterisation of shares as capital assets

- The Tribunal held that the nature of shares must be assessed holistically, taking into account the full history and pattern of holding. The dominant holding of 60% in VSIAPL, held as a strategic long-term investment since March 2012 and consistently classified as ‘investments in subsidiaries’ in the Assessee’s financial statements, determines the character of the asset.

- Revenue’s approach of recharacterizing the entire holding as a trading asset solely on account of the subsequent acquisition of the remaining 40% stake in 2018, without holistic examination of the Assessee’s intent and conduct, was held to be untenable. The Tribunal held that a narrow, transaction-specific view that ignores the earlier and dominant holding is not a permissible basis for recharacterization.

- Once the shares are established as capital assets, the Tribunal held there is no further basis to question the applicability of Section 47(iv). The sole remaining inquiry is whether the two statutory conditions of that provision are fulfilled.

- Applicability of Section 47(iv)

- The Tribunal held that it was undisputed that the Assessee held 100% of both VIPL and VSIAPL and that both are Indian companies, thus transfer of capital assets by the assessee to its subsidiaries will satisfy both conditions of Section 47(iv). Accordingly, the Tribunal upheld the exemption under Section 47(iv) and directed the addition made by the AO to be deleted in its entirety.

- The Tribunal observed that the impugned transaction resulted in a reorganisation of shareholding without any change in ultimate beneficial ownership, with the capital asset continuing to exist in India, thereby indicating continuity of economic interest. Further, there was no material to suggest the transaction was circular, self-cancelling, or devoid of real economic effect.

- Commercial expediency and the ‘armchair businessman’ principle

- The Tribunal reiterated the well-settled principle that Revenue cannot sit in the armchair of a businessman and dictate how business decisions are to be taken. The choice of implementing a group reorganisation through a share transfer followed by a fast-track merger under Section 233 of the Companies Act, 2013 is a legitimate commercial decision and cannot be second-guessed by the Revenue.

- The AO’s contention that a direct merger could have been effected without the prior share transfer, rendering the transaction unnecessary, was rejected. A transaction carried out within the framework of applicable law, without misuse or abuse of any provision of the Act, cannot be characterised as a colourable device merely because an alternative restructuring route existed.

- The existence of a tax benefit, by itself, cannot lead to the conclusion that a transaction is impermissible, unless it is demonstrated that the arrangement lacks commercial substance or is carried out in a non-genuine manner. No such finding was made on the facts.

- Valuation and post-merger accounting disclosures

- The Tribunal held that an assessee has a statutory right to adopt either the Discounted Cash Flow (DCF) or the Net Asset Value (NAV) method. The AO’s rejection of the DCF valuation by mere comparison with the NAV figure, without identifying any specific defect or inaccuracy in the projections or methodology, was held to be procedurally impermissible.

- It is settled law that the AO cannot reject a valuation report without pointing out specific deficiencies therein. Since the AO neither called for further details on the valuation nor recorded any finding on the DCF projections, the allegation of inflated or beneficial pricing was found to lack merit.

- The post-merger accounting disclosure in VIPL’s financial statements, describing VSIAPL shares as ‘cancelled and extinguished’ with the net asset surplus credited to capital reserve, reflects standard accounting treatment required under applicable accounting standards. Such entries in the Indian subsidiary’s books cannot constitute evidence that the principal transaction was non-genuine or designed for fund repatriation.

Conclusion

The Chennai ITAT dismissed the Revenue’s appeal and held that the transfer of shares in VSIAPL to its wholly owned Indian subsidiary VIPL is a bona fide transfer squarely covered by Section 47(iv) of the Act. The Tribunal affirmed that the shares constituted capital assets on a holistic reading of the Assessee’s holding history, that both statutory conditions of Section 47(iv) were undisputedly satisfied, and that the Revenue had produced no evidence of sham, lack of commercial substance, or misuse of the provisions of the Act. The addition made by the AO was directed to be deleted and the exemption claimed by the Assessee was upheld in full.

Kretha Comments

The ruling affirms that the characterisation of shares held as long-term strategic investments is not displaced by the subsequent acquisition of a residual stake in the same entity, particularly where the dominant holding was consistently treated as an investment in the assessee’s financial statements over several years.

The Tribunal’s restatement of the ‘armchair businessman’ principle is significant in the context of intra-group restructurings. The operational choice between a direct merger and a two-step process involving a share transfer followed by a fast-track merger falls within the domain of commercial judgment. Provided the transaction is carried out within the framework of law and is not demonstrated to be circular or devoid of economic substance, it cannot be disregarded on account of a perceived tax advantage alone. This has broader implications for reorganisations undertaken by multinational groups with Indian subsidiaries.

The ruling also reinforces that the AO’s power to examine a valuation report does not extend to a blanket rejection of the DCF methodology without engaging with the underlying assumptions and projections.

- IT(TP)APPEAL NO. 63 (CHNY) OF 2023 ↩︎

Leave A Comment