Background of the case

In a significant ruling, the Mumbai Income Tax Appellate Tribunal (‘ITAT’), in the case of Fairbridge Capital (Mauritius) Limited1, has delivered an important judgment clarifying the scope and applicability of Section 56(2)(x) of the Income-tax Act, 1961 (‘the Act’) in the context of conversion of Optionally Convertible Cumulative Redeemable Preference Shares (‘OCCRPS’) into equity shares.

The ruling addresses fundamental questions relating to the meaning of ‘consideration’ under Section 56(2)(x), the treatment of natural capital appreciation in convertible instruments, and the interplay between anti-avoidance provisions and the legislative framework governing tax-neutral conversions under Section 47(xb) of the Act.

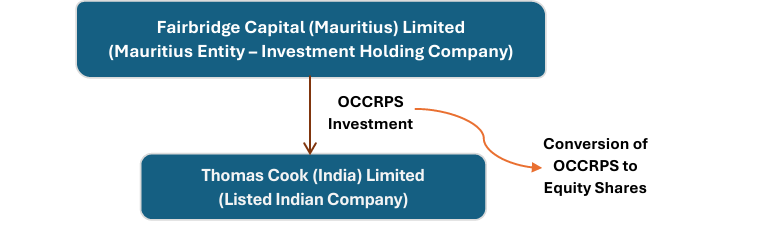

Transaction structure

Facts of the case

- Fairbridge Capital (Mauritius) Limited (‘the Assessee’), a Mauritius-incorporated investment holding company, was allotted 43,56,57,000 OCCRPS of Thomas Cook (India) Limited (‘TCIL’), a listed entity, on 02 April 2021 at INR 10 per share on a private placement basis.

- At the time of issuance, the fair market value of TCIL’s equity shares was INR 47.30 per share, and the terms of issuance expressly provided that the OCCRPS shall be converted into equity shares at a predetermined price of INR 47.30 per equity share within eighteen months from the date of allotment.

- On 03 February 2022, TCIL’s Board approved the conversion of 30,27,20,000 OCCRPS at the predetermined price of INR 47.30 per equity share, and pursuant thereto, the Assessee was allotted 6,40,00,000 equity shares on 17 March 2022.

- The Assessing Officer computed the fair market value of the equity shares received on conversion at INR 66.15 per share in terms of Rule 11UA and proposed to tax the difference between INR 66.15 and INR 47.30 (i.e., INR 18.85 per share) under Section 56(2)(x), resulting in a proposed addition of INR 1,20,64,00,000.

- The Dispute Resolution Panel (‘DRP’) confirmed the proposed addition.

- Aggrieved, the Assessee filed an appeal before the Mumbai ITAT challenging the invocation of Section 56(2)(x) on the conversion of OCCRPS into equity shares.

Key Issues

- Whether conversion of OCCRPS into equity shares constitutes receipt of property for “inadequate consideration” under Section 56(2)(x).

- Whether the predetermined conversion price (INR 47.30 per share) can be regarded as “consideration” for purposes of Section 56(2)(x).

- Whether valuation under Rule 11UA can independently justify an addition where the foundational condition of “inadequate consideration” is not satisfied.

Key Takeaways

1. Section 56(2)(x) is an anti-abuse provision, not a general charging provision

- The ITAT held that Section 56(2)(x) is a deeming provision introduced with a narrowly tailored anti-abuse object to bring to tax receipts of property where there is a clear element of gratuitous enrichment or colourable value shifting, camouflaged as a transaction.

- Being a provision which creates a tax incidence by legal fiction, the ITAT held that its application must be strictly confined to the conditions expressly stipulated therein and cannot be stretched to tax legitimate conversions or exchanges where property is surrendered for property received.

- The ITAT emphasized that what is sought to be taxed as ‘income from other sources’ cannot, by a side wind, be the natural appreciation of a capital asset, especially when the Act itself provides a distinct code for taxation of capital gains.

2. ‘Consideration’ means the value of property surrendered at conversion, not the predetermined conversion price

- The ITAT held that the predetermined conversion price of INR 47.30 per equity share is not the ‘consideration’ for Section 56(2)(x) purposes rather it is a regulatory construct embedded at the time of issuance, fixed in compliance with SEBI ICDR Regulations, governing the conversion ratio and forming the basis for cost of acquisition under Section 49(2AE).

- The ITAT held that on the date of conversion, the Assessee surrenders OCCRPS (capital instruments whose value is intrinsically linked to underlying equity shares), not monetary consideration, and therefore, the consideration for receipt of equity shares is the value of the preference shares surrendered at the point of conversion.

- The ITAT relied on the Supreme Court decision in Reva Investment (P.) Ltd. v. CGT2 to emphasize that inadequacy of consideration must be examined in a broad commercial sense, and where property is exchanged for property, the valuation of what is given and what is received must be undertaken on a similar basis.

3. ‘Aggregate’ comparison requires holistic, contemporaneous valuation

- The ITAT held that Section 56(2)(x) mandates a comparison between the ‘aggregate’ fair market value of property received and the ‘aggregate’ consideration, indicating a holistic, contemporaneous and value-consistent comparison at the point of receipt.

- In the present case, when the aggregate value of the OCCRPS surrendered is compared with the aggregate value of equity shares received on conversion, on a consistent valuation plane and at the same point of time, there is no inadequacy of consideration.

4. Invocation of Section 56(2)(x) would lead to double taxation and violate the legislative scheme

- The ITAT ruled that if the Revenue’s interpretation were accepted, capital appreciation embedded in a convertible instrument would be taxed first as income from other sources at conversion and thereafter subjected to capital gains tax upon eventual transfer, resulting in layered taxation of the same economic increment, which is alien to the scheme of the Act.

- The ITAT held that such interpretation would be destructive of the legislative choice embodied in Section 47(xb), which consciously defers taxation of such appreciation until a subsequent taxable transfer.

- It further held that Section 49(2AE) reinforces that appreciation embedded in preference shares remains within the capital field and is to be taxed only upon a subsequent taxable transfer.

5. Rule 11UA is a machinery provision and cannot create a charge where none exists

- The ITAT held that valuation rules are machinery provisions which neither create a charge nor expand the scope of a charging provision; they merely provide a method for determining fair market value once the conditions of Section 56(2)(x) are otherwise satisfied.

- The ITAT emphasized that the charging condition under Section 56(2)(x) must first be satisfied on a proper interpretation of ‘consideration’, and only thereafter does the question of valuation arise.

Conclusion

The Mumbai ITAT allowed the appeal of the Assessee and directed the deletion of the entire addition of INR 1,20,64,00,000 made under Section 56(2)(x) of the Act. It held that conversion of OCCRPS into equity shares does not result in receipt of property for inadequate consideration, as the consideration is represented by the value of the OCCRPS surrendered at the time of conversion.

Kretha Comments

The Mumbai ITAT’s decision in Fairbridge Capital is a landmark ruling that provides much needed clarity on the scope and applicability of Section 56(2)(x) in the context of conversion of convertible instruments.

The ruling reinforces the principle that Section 56(2)(x) is an anti-abuse provision and cannot be invoked to tax legitimate capital appreciation embedded in structured instruments.

For investors, the decision provides critical clarity that conversion of convertible securities when undertaken within the regulatory framework remains within the capital field and cannot be recharacterized as income from other sources.

Leave A Comment